Which Foreign Communities Hold the Largest Private Wealth in the Emirates?

The United Arab Emirates has become one of the world’s most important centres for international wealth, entrepreneurship and cross-border capital. Over the last two decades, Dubai and Abu Dhabi have moved beyond their traditional roles as trade and logistics hubs to become preferred destinations for global entrepreneurs, family businesses, high-net-worth individuals and expatriate investors.

This shift is visible in real estate ownership, company formation, banking activity, trade networks and private wealth relocation. The UAE is no longer simply a place where expatriates work. For many foreign communities, it has become a long-term capital base.

According to BCG’s 2026 Global Wealth Report, cross-border wealth booked in the UAE reached approximately **$721 billion in 2025**, making the country one of the fastest-growing global wealth booking centres. The development of the Dubai International Financial Centre, Abu Dhabi Global Market, long-term residency options, tax competitiveness and a strong business infrastructure have helped the UAE attract capital from Asia, Europe, the Middle East and Africa.

However, understanding who has invested most heavily in the UAE requires a different lens from traditional foreign direct investment data. Official FDI statistics measure capital flows into companies and productive assets. They do not fully capture expatriate-owned property, bank deposits, family businesses, private companies, trading assets, or wealth held through free-zone structures and family offices.

This Institute of Customer Management (ICM) Insight therefore looks at cumulative private and diaspora-linked assets in the UAE. The estimates below combine available evidence from Dubai property ownership data, business registration trends, diaspora size, reported asset estimates, and broader wealth-centre analysis.

These figures should be read as **indicative ranges**, not audited figures. The UAE does not publish a complete nationality-by-nationality breakdown of private bank deposits, beneficial ownership of companies, free-zone assets or family wealth. As a result, any ranking of total foreign community wealth must be based on triangulation rather than a single official dataset.

1. India: scale, labour-market depth and the largest aggregate capital base

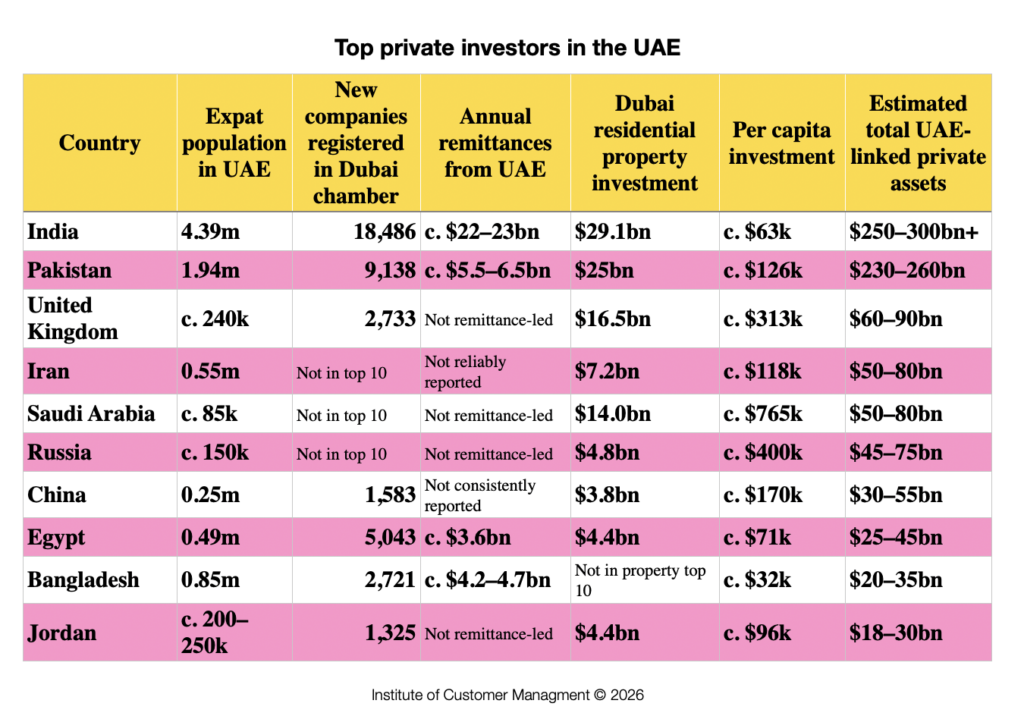

India is the clear number one foreign community in the UAE by population, business formation and aggregate economic footprint. The Indian Ministry of External Affairs lists approximately 4.34 million Overseas Indians in the UAE as of January 2026, making the UAE one of the largest Indian diaspora centres in the world. The Indian Embassy in Abu Dhabi also describes Indians as the UAE’s largest expatriate community, representing roughly 35% of the country’s population.

The post-pandemic period appears to have strengthened India’s demographic and labour-market position in the UAE. During COVID-19, many expatriate workers across the Gulf experienced job losses, salary cuts and return migration. Research on Indian migrant workers in the UAE found that the pandemic transformed employment status and reduced income and remittance flows for many workers.

As the UAE economy reopened, employers in sectors such as construction, logistics, retail, hospitality, delivery services, facilities management, back-office operations and technical services needed to rebuild workforces quickly and cost-effectively. India was well placed to supply lower wage, both skilled and semi-skilled labour because of the scale of its labour market, established recruitment channels, English-language capability, large existing diaspora networks and familiarity with Gulf employment systems.

This does not mean that all Indian workers are low-paid. The Indian community is highly diverse. The Indian Embassy notes that the community’s profile has changed substantially over time: while in the 1970s and 1980s the Indian community was overwhelmingly blue-collar, today around 35% of the Indian community consists of professionally qualified personnel, businesspeople, white-collar non-professionals and their families.

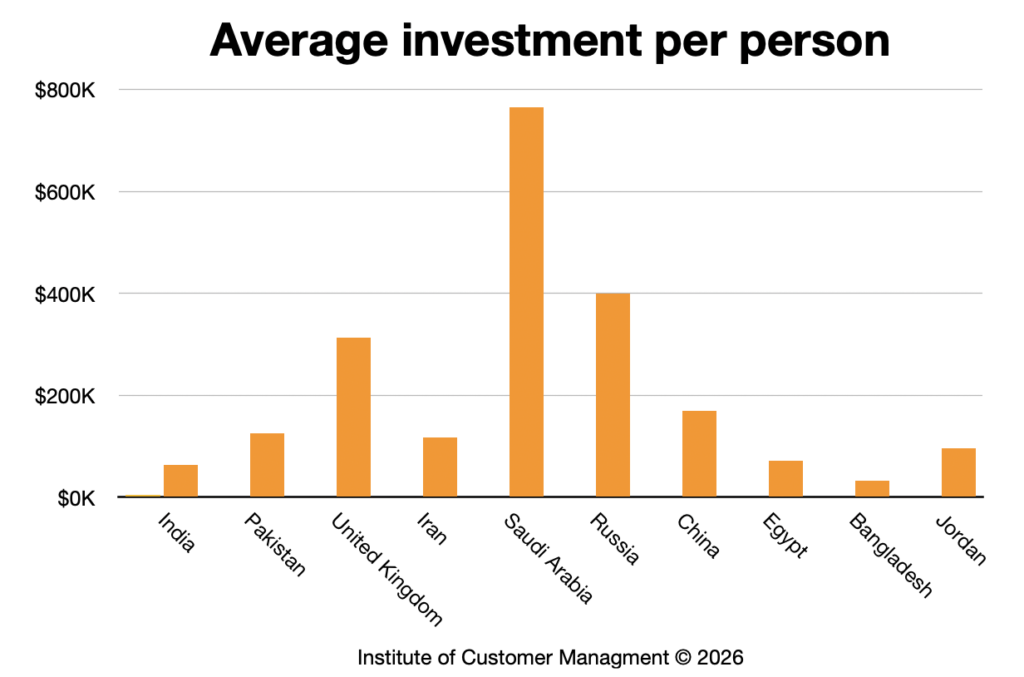

However, India’s very large population base means that its per-capita investment profile is likely lower than that of smaller but wealthier foreign communities such as the British, Saudis, Iranians or Pakistani-origin investors. India’s total UAE-linked asset base is large because the community is large.

Indian capital in the UAE comes from three layers: first, mass employment and savings; second, SMEs and trading companies; and third, major Indian-owned corporate groups and high-net-worth families.

Business formation data reinforces this. In H1 2025, Indian-owned companies were the largest group of new non-UAE companies joining Dubai Chamber of Commerce, with 9,038 new Indian companies, representing 14.9% year-on-year growth. This placed India far ahead of Pakistan, Egypt, Bangladesh, the UK and China in new company formation.

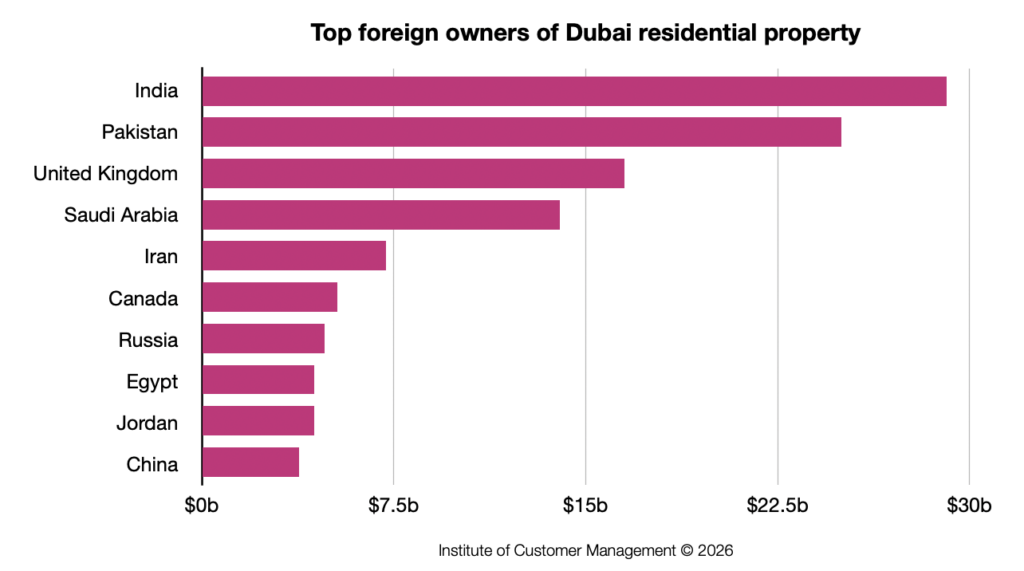

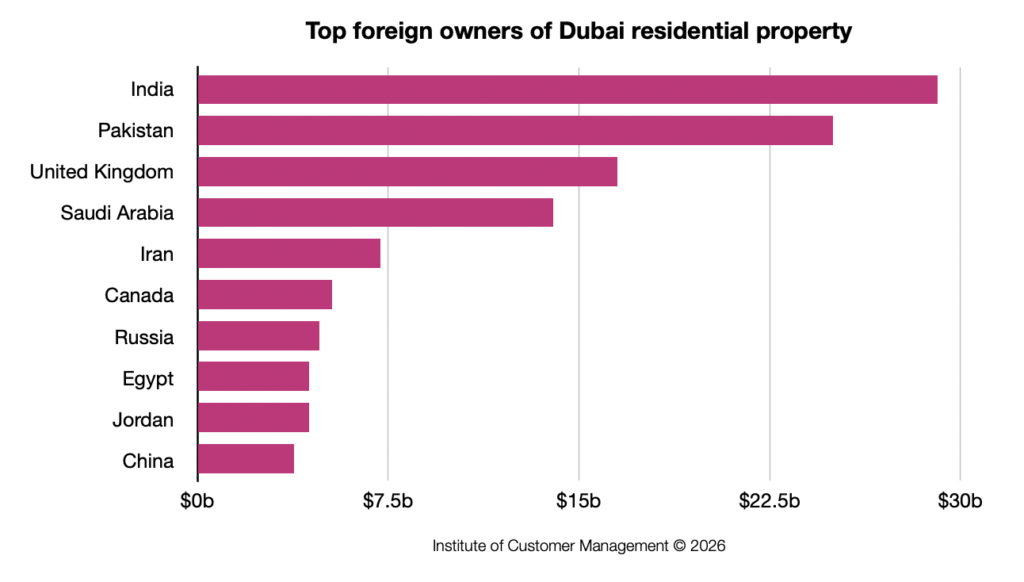

The strongest property evidence also confirms India’s leadership. Dubai residential property research has placed Indian nationals as the largest foreign owners of Dubai residential real estate. In the 2022 dataset, Indian-owned existing and off-plan residential property in Dubai was valued at approximately $29.1 billion.

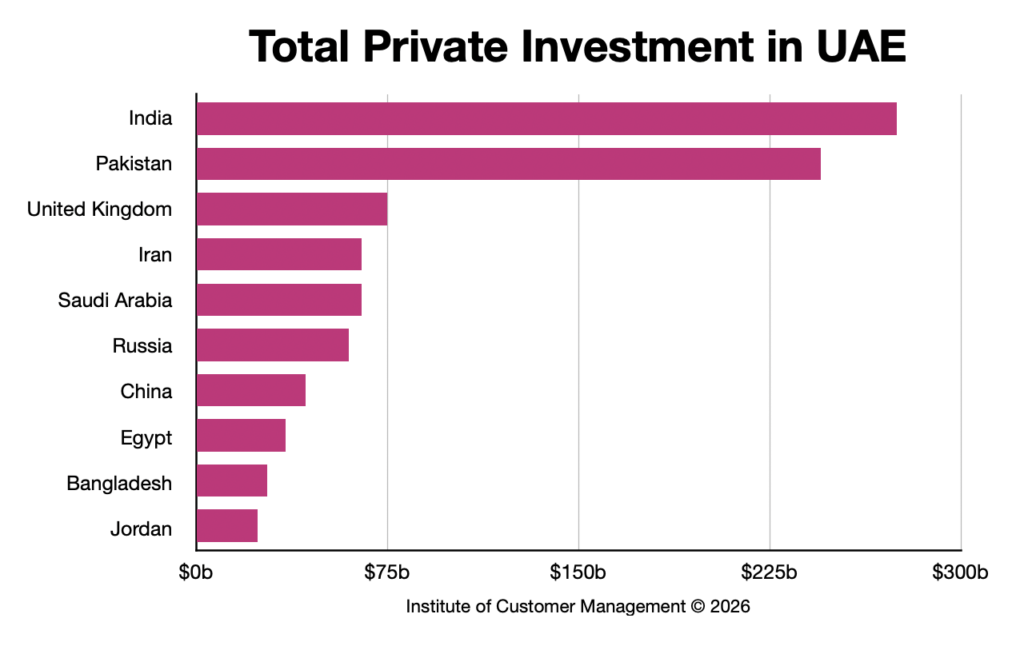

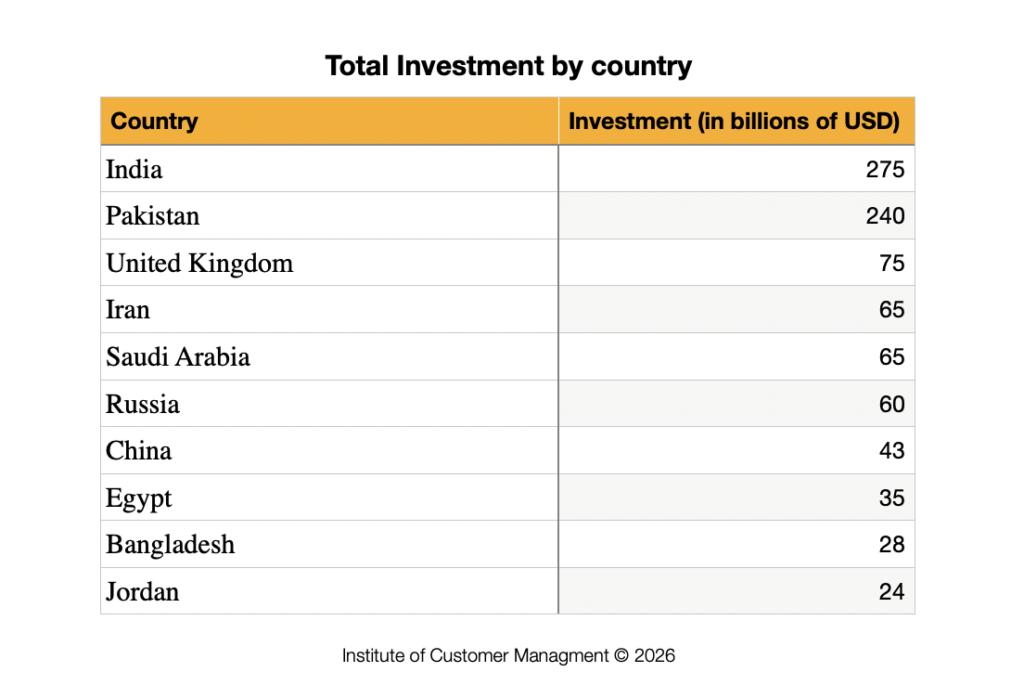

On a cumulative basis, Indian-linked private assets in the UAE are likely in the range of $250–300 billion+. However, because this wealth is spread across more than four million residents, India’s per-capita asset intensity is likely lower than that of Pakistan, the United Kingdom, Saudi Arabia, Iran or Russia.

India should therefore be understood as the UAE’s largest aggregate foreign capital community, but not necessarily the highest per-capita capital community.

2. Pakistan: a large but under-measured capital base

Pakistan is the second-largest foreign community by cumulative private assets in the UAE. This is not only a contemporary investment story. It is also rooted in one of the UAE’s oldest international relationships.

Pakistan was among the first countries to establish diplomatic relations with the UAE after the federation was founded in 1971. The relationship predates many of the UAE’s modern economic institutions and has historically included diplomacy, defence cooperation, aviation, labour migration, trade and private-sector investment.

Pakistani involvement in the early development of the UAE was particularly significant. Pakistani officers helped support the development of the Emirates’ armed forces, especially in the early air force. Pakistan also played an important role in the early operational development of Emirates Airline, with PIA providing aircraft, pilots and operational support during the airline’s launch phase. This history created a deep institutional and people-to-people relationship between the two countries.

Pakistan’s private capital footprint in the UAE is therefore best understood as the product of several decades of migration, entrepreneurship, property ownership and business formation. The Pakistani community was among the early expatriate communities to help build the UAE’s labour force, commercial base and service economy. Over time, this presence evolved from employment and remittances into property ownership, trading companies, SMEs, professional services, family businesses and private wealth accumulation.

A widely cited 2018 estimate presented to Pakistan’s Supreme Court suggested that Pakistanis held approximately $150 billion in UAE properties and assets. This figure appears to have referred to total assets rather than property alone, meaning it likely included real estate, businesses, bank balances, trading companies and other private holdings.

Since 2018, the UAE’s financial and property markets have expanded significantly. UAE bank deposits, Dubai property values, free-zone activity and private business formation have all grown substantially. Pakistani business formation has also remained strong: in 2025, Pakistan ranked second among foreign nationalities for new companies joining Dubai Chamber of Commerce, with 9,138 new Pakistani companies registered during the year.

There is also evidence of a new phase of Pakistan-linked real estate investment in Dubai. Bahria Town, Pakistan’s largest real estate developer, through BT Holding / BT Properties, has confirmed a major mixed-use community in Dubai South. The project is expected to cover more than 20 million square feet, reflecting the growing ambition of Pakistani real estate capital to participate directly in Dubai’s next phase of urban development.

The current estimate for Pakistani nationals’ cumulative private assets in the UAE is approximately $230–260 billion.

This figure may still be conservative. A significant amount of Pakistani-origin wealth may be recorded under other nationalities, particularly where overseas Pakistanis hold British, American, Canadian, Australian or European dual passports. These investors may buy Dubai property, establish free-zone businesses, open bank accounts or hold private assets in the UAE under their current citizenship rather than under Pakistani nationality.

If overseas Pakistani-origin investors are included, the broader Pakistan-linked UAE asset base could exceed $300 billion.

3. The United Kingdom: property, professional wealth and tax-driven relocation capital

The UK is one of the most important non-Asian sources of private wealth in the UAE. British nationals are major owners of Dubai property, and the UAE has become a preferred relocation destination for entrepreneurs, finance professionals, consultants, retirees and high-net-worth families.

In recent years, this trend appears to have accelerated. A combination of UK tax and cost pressures has made the UAE more attractive for wealthy British nationals and internationally mobile families. From 1 January 2025, private school education and boarding services in the UK became subject to VAT at the standard rate of 20%.

Property taxation has also become a factor. For buyers of additional residential property in England and Northern Ireland, higher Stamp Duty Land Tax rates apply where a purchaser will own more than one residential property. From April 2025, the higher-rate SDLT bands start at 5% and rise to 17%, with an additional 2% surcharge also applying to non-UK resident buyers. These are some of the factors which have driven British citizens to sell of their UK properties, and move to the UAE, which offers excellent international schooling a lower costs than the UK.

For globally mobile British families, these changes sit alongside wider concerns about taxation, wealth planning, inheritance tax exposure, school fees, property costs and business competitiveness. The UAE’s appeal is therefore not only lifestyle-based. It is increasingly linked to tax efficiency, asset protection, international schooling, business continuity and long-term family planning.

This wider trend is also reflected in global wealth-migration analysis. Henley & Partners’ 2025 Private Wealth Migration Report highlights the UAE as one of the key tax-friendly jurisdictions attracting affluent individuals, while identifying Dubai as one of the expanding global wealth hubs for high-earning executives.

In the Dubai residential property dataset, UK nationals were among the largest foreign owners. The value of UK-owned existing and off-plan residential property in Dubai was estimated at approximately $16.5 billion in 2022 (this was before the tax changes in the UK).

Taking property, professional wealth, business ownership, high-net-worth relocation and recent tax-driven migration into account, UK-linked private assets in the UAE are likely in the range of $60–90 billion, with the upper end of this range becoming more plausible if recent relocation trends continue.

4. Iran: sanctions, trade dependency and the UAE as a safe capital base

Iran is one of the most important — and most complex — foreign capital communities in the UAE. Its position is rooted in geography, history and necessity. Dubai has long served as a commercial bridge between Iran and the wider global economy, particularly when sanctions limited Iran’s direct access to international banking, trade finance, shipping, technology and dollar-based transactions.

The UAE’s role in Iranian commerce is not new. Reuters has reported that Persian merchants helped shape Dubai’s trading community from the late nineteenth century, while the 1979 Iranian Revolution created a further wave of Iranian migration and business relocation into Dubai. Over time, this created a deep Iranian commercial ecosystem across trading, shipping, wholesale, exchange houses, property and private companies.

Sanctions have made this relationship more important, but also more sensitive. For many Iranian entrepreneurs, families and companies, the UAE has offered a relatively stable environment to hold assets, conduct regional trade, access international markets and protect wealth from inflation, currency depreciation and domestic political risk. At the same time, sanctions have increased regulatory scrutiny on Iran-linked activity, especially where transactions involve sanctioned entities, front companies, petroleum trade, exchange houses or links to the Iranian state. The US Treasury has previously sanctioned UAE-based companies accused of facilitating Iranian petroleum and petrochemical sales, showing that some Iran-linked commercial channels carry significant compliance risk.

Dubai’s importance to Iran is also visible in trade flows. Recent reporting has described the UAE as a critical gateway for Iran’s imports and re-export activity, with Emirati exports to Iran rising from around $5.2 billion in 2018 to roughly $23 billion in recent years. Iran’s non-oil exports to the UAE also increased from about $5.7 billion to nearly $8 billion.

In property, Iranian nationals are among the major foreign owners of Dubai residential real estate. The EU Tax Observatory’s 2022 dataset estimated Iranian-owned existing and off-plan residential property in Dubai at approximately $7.2 billion. This figure captures property only; it does not include trading companies, bank deposits, private businesses, family wealth, free-zone structures or assets held through other nationalities or corporate vehicles.

For this reason, Iran’s total UAE-linked private asset base is likely far larger than its property holdings alone. A reasonable estimate is $50–80 billion in cumulative Iran-linked private assets in the UAE. The upper end of this range becomes plausible when banking, trade capital, company ownership, family wealth and sanctions-driven asset relocation are included.

Iranian-linked capital should therefore be understood differently from Indian, Pakistani or British capital. It is not only a diaspora wealth story. It is also a sanctions-adaptation story. The UAE has functioned as a commercial pressure valve for Iranian businesses and families seeking access to liquidity, markets, property ownership and international mobility.

5. Saudi Arabia: Gulf family wealth, regional diversification and the UAE–Saudi capital corridor

Saudi Arabia is one of the most important Gulf sources of private capital in the UAE. Unlike Pakistan, India or Bangladesh, the Saudi story is not primarily about labour migration or expatriate remittances. Unlike Iran, it is not primarily a sanctions story. Saudi investment in the UAE is best understood as a regional wealth diversification strategy driven by family capital, second-home ownership, luxury property, corporate links, private equity, family offices and cross-border Gulf business networks.

Saudi nationals have long viewed Dubai and Abu Dhabi as natural extensions of the Gulf investment landscape. The UAE offers proximity, lifestyle, liquidity, international connectivity, private banking access, high-end real estate, and a globally recognised business environment. For many Saudi families, the UAE is not a foreign market in the same way that London, New York or Singapore might be. It is a neighbouring Gulf hub that can be accessed quickly and used for property, leisure, business structuring, investment management and international education.

The strongest hard-data anchor is Dubai property ownership. The EU Tax Observatory’s 2022 dataset estimated Saudi-owned existing and off-plan residential property in Dubai at approximately $14 billion, placing Saudi Arabia among the largest foreign owner groups in Dubai residential real estate. This property figure is important, but it captures only one part of the Saudi footprint. It does not include private companies, bank balances, investment portfolios, family-office assets, corporate holdings, or assets held through UAE companies and other structures.

Saudi-UAE economic integration is also unusually deep. Reuters reported that Emirati-Saudi non-oil bilateral trade reached approximately $41.3 billion in 2024, up from $37.3 billion in 2023, and that Saudi Arabia is the UAE’s largest trading partner in the Arab world. This matters because private wealth rarely moves in isolation. Trade, logistics, procurement, contracting, tourism, property and family business networks create the channels through which Saudi-linked capital is held and reinvested in the UAE.

At the same time, Saudi Arabia is no longer simply exporting capital to the UAE. Under Vision 2030, the Kingdom is trying to retain more capital domestically and position Riyadh as a competing regional business hub. Saudi Arabia’s regional headquarters programme, which took effect from January 2024, requires many international firms seeking Saudi government contracts to establish a regional headquarters in the Kingdom. Reuters described this as part of Saudi Arabia’s push to compete with Dubai for regional business activity.

This creates a more nuanced investment picture. On one hand, some corporate activity that historically sat in Dubai may shift toward Riyadh, especially where companies are targeting Saudi government contracts, giga-projects or Vision 2030-linked opportunities. On the other hand, the UAE remains highly attractive for Saudi private wealth because it offers international connectivity, established financial infrastructure, lifestyle appeal, property liquidity, and a mature wealth-management ecosystem.

Saudi Arabia’s own market reforms may also affect future flows. The Kingdom has moved to open parts of its real estate market to non-Saudi ownership under a more structured regulatory framework, with the Real Estate General Authority describing the updated law as part of the Kingdom’s effort to enhance investment appeal and support Vision 2030. This could encourage more capital to remain inside Saudi Arabia or attract foreign capital into Saudi property. However, it is unlikely to replace the UAE’s role. A more realistic outcome is a dual-hub model, where Saudi Arabia becomes the region’s largest domestic growth market while the UAE remains the region’s most international private-wealth and lifestyle hub.

Saudi-linked private assets in the UAE are therefore likely to be significant and persistent. Based on property ownership, Gulf family wealth, business ties, private banking, and the wider Saudi-UAE economic corridor, a reasonable estimate is $50–80 billion in cumulative Saudi-linked private assets in the UAE.

The strategic issue is not whether Saudi capital will leave the UAE. The more important question is how Saudi families and companies will divide capital between two increasingly important Gulf hubs: Dubai and Abu Dhabi for international wealth, liquidity and lifestyle; Riyadh, Jeddah and Saudi giga-projects for domestic growth and Vision 2030 opportunity.

6. Russia: post-war wealth relocation, sanctions pressure and Dubai as a neutral capital base

Russia has become one of the most important new sources of private capital into the UAE since the full-scale invasion of Ukraine in 2022. Unlike India or Pakistan, Russia’s UAE-linked asset growth is not primarily a long-term diaspora story. Unlike Saudi Arabia, it is not mainly a regional diversification story. Russia is best understood as a geopolitical wealth relocation story.

After Western sanctions were imposed on Russia, many wealthy Russians, entrepreneurs and internationally mobile families began looking for jurisdictions where they could preserve capital, access banking and property markets, maintain mobility, and avoid the freezing of assets in Europe. Reuters reported in March 2022 that rich Russians were trying to shift wealth from Europe to Dubai to protect assets from the tightening sanctions environment. Dubai’s appeal was strengthened by the UAE’s international connectivity, luxury property market, business infrastructure and relatively neutral diplomatic positioning.

The impact was quickly visible in real estate. Reuters reported that wealthy Russians were buying property in the UAE and Turkey as a shelter from sanctions, with some buyers seeking homes and others buying for investment. Later in 2022, Dubai property sales surged, and Betterhomes data cited by Reuters showed Russian buyers increasing by 164% in the first half of 2022 compared with the first half of 2021.

The strongest empirical estimate comes from the EU Tax Observatory’s Dubai housing-market research. It found a substantial boom in Russian interest after the Ukraine invasion, with Russian-linked residential leases and utility accounts rising sharply. Using conservative assumptions, the researchers estimated that Russians bought up to $2.4 billion of existing properties and a further $3.9 billion of in-development properties after the invasion — around $6.3 billion in post-invasion purchases.

This figure is property only. It does not include bank deposits, private companies, family offices, trading structures, yachts, investment vehicles, free-zone companies or assets held through second citizenships. It also does not capture Russian-origin wealth held through Cyprus, Caribbean, European, Turkish or Israeli passports, or through corporate entities. Therefore, Russia’s total UAE-linked asset base is likely significantly larger than the property data alone.

Russian capital in the UAE should also be treated as heterogeneous. It includes ultra-high-net-worth individuals, sanctioned or politically exposed individuals, entrepreneurs, technology professionals, commodity traders, family offices and middle-class Russians seeking relocation. Some of this capital is lawful private wealth seeking stability; some is sanctions-sensitive and subject to enhanced compliance scrutiny.

The sanctions risk is material. Western governments have increasingly scrutinised Russia-linked networks operating through third countries. The US State Department has described Russian procurement networks using intermediaries and companies based in jurisdictions including the UAE to evade sanctions. Reuters has also reported on Russian corporate and energy-linked activity shifting through Dubai-based structures, including Lukoil setting up a new oil-trading arm in Dubai after sanctions pressure affected related entities.

This creates a two-sided investment story. On one side, the UAE has benefited from Russian private capital moving into property, services, hospitality, retail, trading, finance and family wealth management. On the other side, Russian-linked capital brings higher due-diligence requirements for banks, real estate brokers, professional services firms and free-zone authorities. The UAE’s challenge is to remain attractive as a global wealth hub while avoiding the perception that it is a sanctions-avoidance centre.

By 2023, Russian buying activity had begun to normalise from the initial surge. Reuters reported that Russians were the top non-resident buyers of Dubai homes in the first quarter of 2023 but had dropped to third place by the end of the year, with Indian and British buyers accounting for the largest share over the full year. This suggests that the initial post-war rush may have cooled, but the stock of Russian capital already placed in the UAE remains significant.

On a cumulative basis, a reasonable estimate for Russia-linked private assets in the UAE is $45–75 billion. The lower end reflects identifiable property, business and relocation capital. The upper end becomes plausible if bank balances, company structures, offshore-held assets, family offices and second-passport Russian-origin wealth are included.

Russia’s role in the UAE capital map is therefore best summarised as follows: the Ukraine war turned Dubai from a luxury destination for wealthy Russians into a strategic wealth-protection and relocation hub.

7. China: trade-platform capital, Dragon Mart and the UAE as a gateway to the region

China’s UAE-linked capital base is different from India, Pakistan, the UK, Iran, Saudi Arabia or Russia. It is not primarily a mass-diaspora wealth story, nor is it mainly a sanctions or tax-relocation story. China’s position in the UAE is best understood as a trade-platform and regional-gateway story.

For Chinese companies, Dubai functions as a commercial bridge into the Middle East, Africa, South Asia and parts of Europe. The UAE’s ports, free zones, logistics infrastructure, business services and re-export networks make it an ideal location for Chinese wholesalers, manufacturers, technology firms, consumer-goods suppliers and trading companies seeking regional distribution.

The clearest symbol of this relationship is Dragon Mart in Dubai. Dragon Mart is widely described as the world’s largest Chinese mall and trading hub for Chinese products outside Mainland China. It hosts thousands of shops and functions not only as a retail destination, but also as a wholesale and distribution platform for Chinese goods moving across the UAE and wider region.

This matters because Dragon Mart represents a different kind of investment footprint. It is not simply about Chinese nationals buying property or opening bank accounts. It is about embedding Chinese supply chains into Dubai’s commercial infrastructure. Through Dragon Mart and similar trade channels, Chinese companies use the UAE as a regional showroom, warehousing point, sales platform and re-export base.

Chinese-owned company formation has also been growing. Dubai Chamber data placed China among the top foreign nationalities for new companies joining Dubai Chamber in 2025. While China’s new-company count is lower than India, Pakistan or Egypt, the strategic value of Chinese firms is significant because they are often linked to trade, logistics, manufacturing, e-commerce, electronics, construction materials, consumer goods, technology and regional distribution.

Property ownership also supports China’s presence, although it is not the main driver of the China story. The EU Tax Observatory’s Dubai property research estimated Chinese-owned existing and off-plan residential property in Dubai at approximately $3.8 billion in 2022. This is meaningful, but much smaller than India, the UK, Saudi Arabia, Pakistan or Iran. The larger Chinese footprint is likely held through trading companies, commercial stock, logistics structures, free-zone entities and regional business operations.

China’s investment logic is therefore highly strategic. The UAE gives Chinese companies access to a politically stable, tax-efficient and globally connected base close to fast-growing markets. For the UAE, Chinese capital supports trade diversification, logistics growth, retail supply chains, e-commerce and the country’s position as a bridge between Asia, the Middle East and Africa.

A reasonable estimate for China-linked cumulative private and business assets in the UAE is $30–55 billion. This includes property, private companies, wholesale trading capital, free-zone businesses, logistics operations, bank balances and trade-linked assets. The figure could rise substantially over time as China-UAE trade deepens and Dubai continues to function as one of China’s most important offshore commercial platforms.

China’s UAE-linked wealth should therefore be understood as supply-chain capital. The key issue is not only how much Chinese individuals own in Dubai, but how deeply Chinese commerce has become embedded in the UAE’s trading and distribution ecosystem.

8. Egypt: professional migration, SME entrepreneurship and the UAE–Egypt capital corridor

Egypt is one of the most important Arab communities in the UAE’s private capital landscape. Unlike India or Pakistan, the Egyptian story is not primarily driven by sheer population scale. Unlike Iran or Russia, it is not primarily a sanctions or geopolitical relocation story. Egypt’s UAE-linked capital base is best understood as a professional, entrepreneurial and services-led wealth story.

Egyptians have long played an important role in the UAE’s professional economy, particularly in education, healthcare, construction, engineering, media, financial services, retail, hospitality, legal services, consulting and public-sector advisory roles. This has created a sizeable middle-class and upper-middle-class Egyptian community with savings, property ownership, business activity and long-term family links to the UAE.

The clearest recent signal is business formation. In 2025, Egypt ranked third among foreign nationalities for new companies joining Dubai Chamber of Commerce, with 5,043 new Egyptian companies registered during the year. This placed Egypt behind only India and Pakistan, and ahead of the United Kingdom, Bangladesh, Syria, China, Jordan, Türkiye and the United States. Dubai Chamber also reported that total new companies joining the chamber reached 71,830 in 2025, lifting active membership to 292,486 by year-end.

This matters because Egypt’s UAE footprint is becoming more entrepreneurial. Egyptian-owned companies are not only small retail or service firms; they increasingly operate across consulting, marketing, food and beverage, logistics, education, technology, real estate brokerage, professional services and regional trading. Dubai gives Egyptian entrepreneurs access to capital, customers, banking infrastructure, free-zone structures, and a regional market that is difficult to replicate inside Egypt.

Remittances also show the scale of the economic relationship. Egypt Today reported that remittances from Egyptians working in the UAE reached approximately $3.6 billion in fiscal year 2024/2025. This does not measure Egyptian assets held inside the UAE, but it confirms the economic weight of the Egyptian community and its continuing role as a source of household income, savings and cross-border capital flows.

A second driver is Egypt’s domestic economic pressure. Egypt has faced currency devaluation, inflation, foreign-currency shortages and debt pressures in recent years. Reuters described the UAE’s $35 billion Ras El Hekma investment deal in 2024 as a major intervention to help Egypt address a chronic foreign-currency shortage and economic pressure. For Egyptian professionals and entrepreneurs, the UAE offers a more stable currency environment, dollar-linked banking exposure, stronger purchasing power, and a platform for holding savings or building companies outside the volatility of the Egyptian pound.

Property is another important, although smaller, part of the story. The EU Tax Observatory’s Dubai housing-market research estimated Egyptian-owned existing and off-plan residential property in Dubai at approximately $4.4 billion in 2022. That is lower than India, the UK, Saudi Arabia, Pakistan and Iran, but it is still significant, especially when combined with businesses, professional savings, bank balances and family assets.

The wider UAE–Egypt relationship also reinforces Egyptian capital formation in the Emirates. Trade between Egypt and the UAE reportedly reached $9.7 billion in 2025, up from $6 billion in 2024, according to reporting based on Egypt’s Central Agency for Public Mobilisation and Statistics. This expanding trade corridor creates opportunities for Egyptian entrepreneurs in distribution, services, logistics, food products, contracting, tourism, consulting and regional business support.

Egypt’s UAE-linked assets are therefore likely to be more broadly distributed than those of some smaller high-net-worth communities. The Egyptian capital base is not concentrated only in luxury property or family offices. It is spread across professionals, SMEs, service firms, property owners, consultants, investors and families using the UAE as a stable regional base.

A reasonable estimate for Egyptian-linked cumulative private assets in the UAE is $25–45 billion. The lower end reflects identifiable property, savings and SME capital. The upper end becomes plausible when professional wealth, business ownership, bank deposits, regional trading activity and family assets are included.

Egypt’s role in the UAE capital map can therefore be summarised as follows: Egypt is not primarily a wealth-flight story; it is a professional and entrepreneurial scale story, strengthened by Egypt’s domestic currency pressures and the UAE’s role as the Arab world’s most important business platform.

9. Bangladesh: labour scale, savings accumulation and rising SME formation

Bangladesh is one of the UAE’s most important South Asian communities, but its capital profile is different from India or Pakistan. Bangladesh’s UAE-linked wealth is not primarily a high-net-worth or luxury property story. It is better understood as a labour-scale, remittance, savings and emerging SME story.

The Bangladeshi community has historically been concentrated in construction, services, facilities management, logistics, domestic work, hospitality, retail and other labour-intensive sectors. This means that Bangladesh may not rank highly in per-capita wealth compared with British, Saudi, Iranian, Russian or Jordanian investors. However, the size of the community and its rising entrepreneurial activity make Bangladesh economically significant.

The strongest recent signal is business formation. In 2025, 2,721 Bangladeshi companies joined Dubai Chamber of Commerce, a 15% year-on-year increase. This placed Bangladesh fifth among foreign nationalities for new companies joining the chamber, behind India, Pakistan, Egypt and the United Kingdom, and ahead of Syria, China, Jordan, Türkiye and the United States. Dubai Chamber also reported that 71,830 new companies joined in 2025, raising active membership to 292,486 by year-end.

This suggests that the Bangladeshi UAE footprint is evolving. The community is not only a labour force; it is increasingly becoming a small-business and service-business community. Bangladeshi-owned companies are likely concentrated in retail, food, transport, small trading, services, manpower supply, cleaning, contracting support, logistics, repair, maintenance and community-facing businesses.

Remittances also show the scale of the economic relationship. Bangladesh Bank data, reported through CEIC, shows UAE-to-Bangladesh remittance flows remain substantial, with UAE remittances recorded at BDT 47.47 billion in January 2026 and an all-time monthly high of BDT 62.53 billion in June 2024. This does not measure Bangladeshi assets retained in the UAE, but it confirms the continuing income and savings power of the Bangladeshi workforce in the Emirates.

Bangladesh’s UAE-linked wealth is therefore likely to be more distributed and less visible than that of wealthier investor groups. It may sit in bank savings, small business ownership, trading stock, labour-contracting firms, family shops, shared property investment, remittance-linked capital and informal community business networks. Much of this wealth may not appear in high-end property datasets, but it still forms part of the UAE’s wider private capital ecosystem.

A reasonable estimate for Bangladesh-linked cumulative private assets in the UAE is $20–35 billion. The lower end reflects savings, SMEs and modest property exposure. The upper end becomes plausible when business ownership, retained earnings, trading capital, bank balances, community enterprises and long-term savings are included.

Bangladesh’s role in the UAE capital map can therefore be summarised as follows: Bangladesh is not a luxury wealth story; it is a scale-and-savings story, increasingly moving from labour participation into small-business ownership.

10. Jordan: professional capital, property ownership and regional business networks

Jordan’s UAE-linked capital base is smaller in population terms than India, Pakistan, Bangladesh or Egypt, but it is economically significant because of the community’s professional profile, property ownership, business networks and regional integration.

Jordanian nationals have long been active in the UAE across education, healthcare, engineering, finance, consulting, construction, real estate, public administration, media, technology and professional services. This gives the Jordanian community a different profile from larger labour-migration communities. Jordan’s UAE-linked capital is likely to be more concentrated in professional income, property, SMEs, family businesses, consulting firms and regional business networks.

The property data is particularly important. The EU Tax Observatory’s Dubai housing-market research found that foreign nationals held around 43% of the value of Dubai residential property, and that foreign-owned residential real estate grew by about $23 billion between early 2020 and early 2022. In the report’s country-level dataset, Jordan appeared as a notable foreign owner group, with estimated Jordanian-owned existing and off-plan residential property in Dubai of around $4.4 billion in 2022.

Jordan also appears strongly in business formation data. In 2025, 1,325 Jordanian businesses joined Dubai Chamber of Commerce, placing Jordan eighth among foreign nationalities for new companies joining the chamber. This put Jordan ahead of Türkiye and the United States in that specific Dubai Chamber ranking.

This combination of property ownership and business formation makes Jordan more important than its population size alone would suggest. Jordanian capital in the UAE is likely concentrated in professional savings, property, consulting companies, contracting, education, healthcare, business services, real estate brokerage, regional trade and family-owned SMEs.

Jordan also benefits from the UAE’s role as a regional platform. For many Jordanian professionals and entrepreneurs, Dubai and Abu Dhabi offer access to higher salaries, stronger purchasing power, a larger client base, regional corporate headquarters, private schools, healthcare networks and more liquid property markets than are available domestically. The UAE functions as both an employment centre and a capital-preservation platform.

A reasonable estimate for Jordan-linked cumulative private assets in the UAE is $18–30 billion. This range is supported by property ownership, professional wealth, company formation, bank savings and regional business activity. Jordan’s total asset base is below that of larger communities such as India, Pakistan, Egypt or Bangladesh, but its per-capita capital intensity is likely higher than Bangladesh and possibly higher than some larger labour-based expatriate communities.

Jordan’s role in the UAE capital map can therefore be summarised as follows: Jordan is a professional-capital story: a smaller community with a relatively strong footprint in property, services, SMEs and regional business networks.

Strategic implications

The UAE’s private capital map reveals three important shifts.

First, the UAE has become a diaspora capital hub. Communities from India, Pakistan, Iran, Egypt, Bangladesh and Jordan do not only remit money home. They also accumulate assets, build businesses and establish long-term financial footprints in the Emirates.

Second, Dubai and Abu Dhabi are now competing directly with traditional wealth centres. The UAE’s rise as a cross-border wealth booking centre reflects not just tax advantages, but also institutional depth, infrastructure, quality of life, global connectivity and perceived political stability.

Third, foreign private wealth in the UAE is increasingly shaped by **mobility and optionality**. Investors are not only seeking returns. They are seeking residency options, business continuity, currency diversification, education access, family security and regional market reach.

Conclusion

The UAE’s foreign private wealth base is broader and deeper than official FDI figures suggest. India and Pakistan appear to dominate the cumulative private asset landscape, followed by major capital communities from the UK, Iran, Saudi Arabia, Russia, China, Egypt, Bangladesh and Jordan.

For policymakers, educators, investors and business leaders, this matters. The UAE is not only a destination for investment. It is a platform where diaspora networks, private wealth, entrepreneurship and global mobility intersect.

As the UAE continues to develop as a global business and wealth hub, understanding the nationality and community structure of its capital base will become increasingly important for market entry, education recruitment, financial services, real estate, entrepreneurship and international partnership strategy.

Methodology note

This ranking is based on an analytical estimate of **cumulative private and diaspora-linked assets in the UAE. It is not a ranking of annual FDI flows.

The estimate considers:

1. Dubai residential property ownership by nationality.

2. Dubai Chamber company formation data by nationality.

3. Expatriate population size.

4. Reported asset estimates where available.

5. The UAE’s role as a cross-border wealth booking centre.

6. Qualitative evidence of trade, family business and private wealth concentration.

The main limitation is data transparency. Bank deposits, private company equity, free-zone holdings, family-office structures, nominee ownership and beneficial ownership are not publicly broken down by nationality. The figures should therefore be treated as informed estimates rather than official audited values.